The Autocorrelation function is one of the widest used tools in timeseries analysis. It is used to determine stationarity and seasonality.

Stationarity:

This refers to whether the series is “going anywhere” over time. Stationary series have a constant value over time.

Below is what a non-stationary series looks like. Note the changing mean.

If a series is non-stationary (moving), its ACF may look a little like this:

On the other hand, observe the ACF of a stationary (not going anywhere) series:

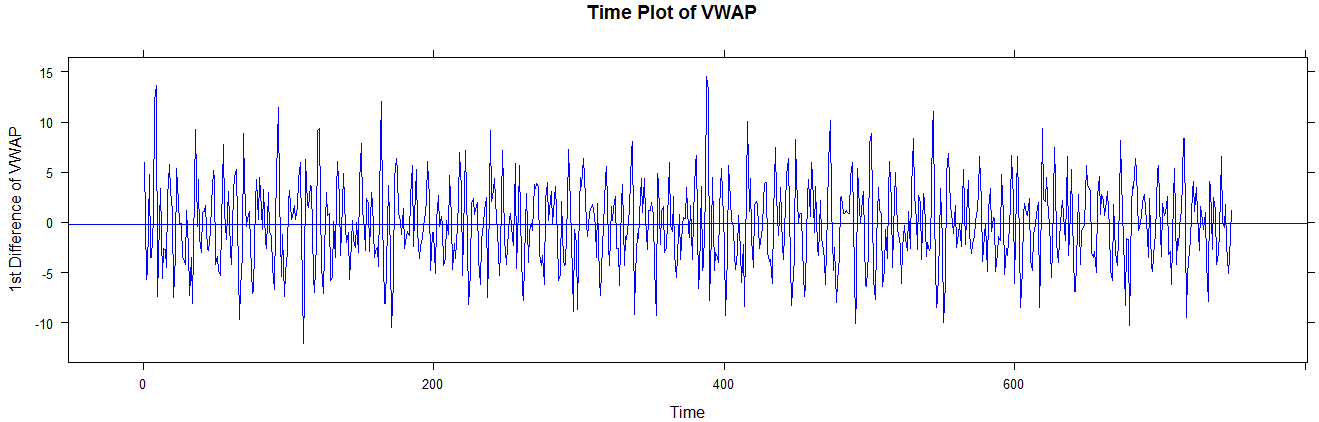

Consider the case of a simple stationary series, like the process shown below:

We do not expect the ACF to be above the significance range for lags 1, 2, … This is intuitively satisfactory, because the above process is purely random, and therefore whether you are looking at a lag of 1 or a lag of 20, the correlation should be theoretically zero, or at least insignificant.

Next: ACF for Seasonality

Abbas Keshvani