Members of the Federal Open Market Committee, the body which decides the Fed’s interest rate policy, have their words closely scrutinized for hints about what the next policy change could be. Aside from the official policy-setting meetings (around eight per year), FOMC members give speeches throughout the year (78 in 2019).

Here I use natural-language processing (NLP) to assign a score to each of those speeches, as well as official FOMC statements.

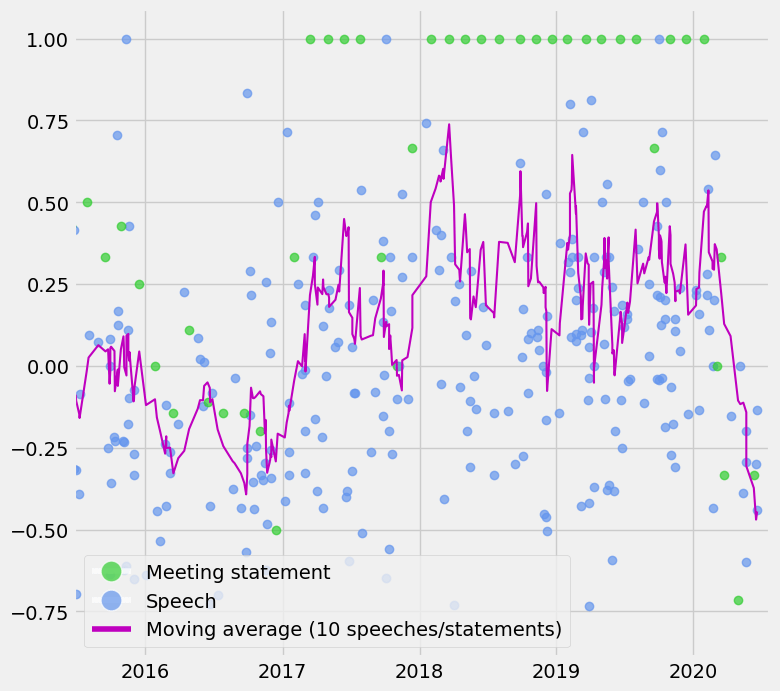

As expected, the index shows that recent Fed speeches have been relatively negative in their tone.

Method:

The formula I use to calculate a speech’s score is based off the number of positive words and negative words in that speech/statement.

A score of +1 means that a speech had only positive words like “efficient”, “strong” and “resilient”, while -1 means it had only negative words like “repercussions”, “stagnate”, and “worsening”. The dictionary I use to determine whether a word is positive is based off (I have modified it) a 2017 paper published by the Federal Reserve Board1.

One also has to account for negation. A statement like “growth is not strong” has a positive word in it (“strong”) which should actually be counted as a negative word. As such, if a positive word is within three words of a negation word like “not” or “never”, then it is treated as a negative word. On the other hand, a negative word near a negation word (“growth is not poor”) is simply not counted, rather than treated as a positive word.

I downloaded the speeches and statements, did the NLP analysis, and produced the charts on Python.

Relation with yields:

Here I chart the Fed sentiment index against the US 2y yields, as well as the sentiment scores of the official meeting statements. The index moved higher from late 2016 to early 2018 as the Fed started hiking policy.

However in early 2018 the sentiment index indicated that the Fed had turned less positive, but yields continued moving higher as the hiking cycle continued. It is also important to note that sometimes a shift in FOMC thinking/language drives market price-action, and sometimes it is the other way round, so one cannot expect the index to always presage higher or lower yields.

As we go into the September FOMC meeting, where some people are expecting the Fed to announce yield curve control, keeping an objective eye on Fed sentiment will become even more important.

Everything done on Python.

References:

1Correa, Ricardo, Keshav Garud, Juan M. Londono, and Nathan Mislang (2017) – Sentiment in Central Banks’ Financial Stability Reports. International Finance Discussion Papers 1203.

Nice article. Something similar, Fed Beige Book sentiments are done by http://www.economyx.ai